Wedding photographer & videographer

insurance, explained.

Most couples find out about wedding photographer insurance the same way: two weeks before the wedding, the venue's event coordinator emails asking for a Certificate of Insurance, and the bride forwards it to the photographer with a question mark in the subject line.

If your photographer has it together, the COI shows up in 48 hours and you never think about it again. If they don't, you're scrambling at the last minute. And some venues will not let an uninsured vendor on the property. We've seen photographers turned away at the door.

Here's what's actually happening behind the paperwork. What coverage looks like for both photographers and videographers, what the venue is asking for, and what to handle on your side before it becomes a problem.

Quick answers

What is a Certificate of Insurance for a wedding photographer?

A Certificate of Insurance (COI) is a one-page document from the photographer's insurance carrier that proves three things: an active general liability policy, a minimum coverage amount (typically $1M per occurrence, $2M aggregate), and the venue listed as a covered party for your specific event date. Real pros pay for insurance year-round; the COI itself is free per request, 24 to 48 hour turnaround.

Does the photographer's insurance cover their wedding videography work?

Only if their policy was underwritten to include both photo and video. Most aren't, by default. If the same vendor shoots your photos and your wedding film, ask explicitly whether their insurance covers both services. The answer should be yes with no hesitation. If they have to think about it, a tripod cable trip or damaged sound system could get denied.

What does "Additional Insured" mean on a wedding COI?

It means your venue is named on the photographer's policy as a covered party for your event. If something goes wrong, a flash overheats, a light stand falls, gear trips a guest, the photographer's insurance protects the venue from being sued. Without this clause, the venue's own insurance has to absorb it, which is why most venues require it.

What is a waiver of subrogation in a wedding photography contract?

Subrogation is when an insurance company pays out a claim and then sues the third party they think actually caused the damage to recover the money. A waiver of subrogation means the photographer's carrier gives up that right against the venue. It's a yes-or-no question on the COI: their carrier either includes it or doesn't.

When should we send our venue's vendor requirements to the wedding photographer?

At venue contract signing, request the vendor requirements document. Forward it to your photographer 90 days out from the wedding. They request the COI from their carrier at 30 days out. The COI lands with your venue's coordinator 14 days out. Confirm it's on file at 7 days out. Wedding day, photographer brings a printed copy as backup.

The three types of insurance that matter for wedding work

Before we get to the COI, it helps to know what's underneath it. A working wedding pro typically carries three different types of coverage, and they're not the same thing.

1. General Liability (GL), covers bodily injury or property damage to OTHER people. A guest trips on your light stand and breaks a wrist. Your flash kit overheats and burns a hole in a venue's tablecloth. Your gear case scratches a marble countertop. GL is what your venue is asking about. Standard minimum is $1M per occurrence, $2M aggregate per year.

2. Equipment Coverage (Inland Marine): covers YOUR gear if it's stolen, dropped, soaked in rain, or otherwise destroyed. This is separate from liability and isn't what venues ask about. It's what protects the photographer's business from getting wiped out by one bad day. Roughly $1,500–$3,000/year for a typical $30K-$60K kit.

3. Errors & Omissions (E&O), covers professional mistakes. Lost photos. Corrupted files. A bride suing because the gallery doesn't include a shot she expected. Some pros carry this; many don't. Venues don't ask about it.

When your venue is asking for "proof of insurance," they're asking about #1. The general liability policy. The Certificate of Insurance (COI) is the document that proves it.

What a Certificate of Insurance actually is

A COI is a one-page document from a working photographer's insurance carrier that proves three things: the photographer has an active general liability policy, the policy meets a minimum coverage amount (typically $1M per occurrence, $2M aggregate), and the venue is listed as a covered party for your specific event date.

A real working pro pays for this insurance year-round. It's part of doing business. The COI itself is just a request to the carrier. They generate one for each venue that asks. There's no extra cost per event. Turnaround is usually 24–48 hours.

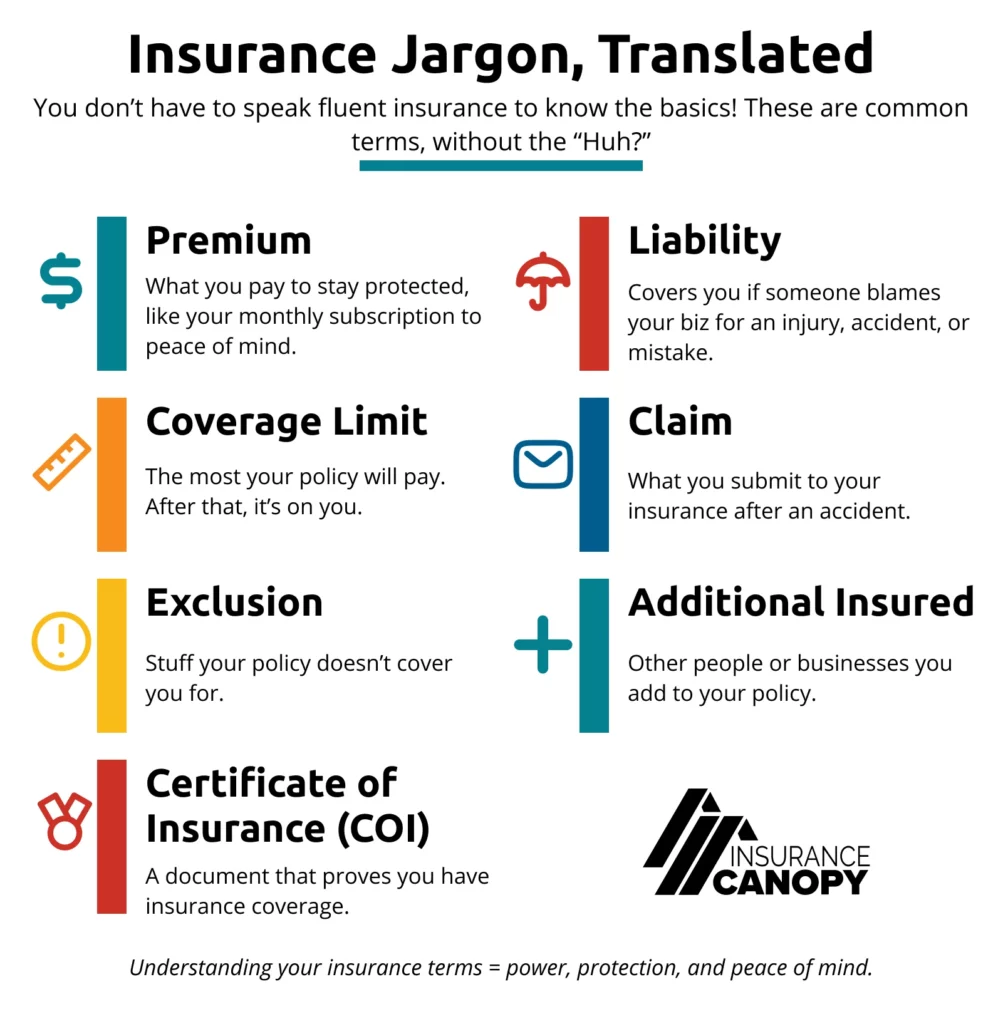

Insurance jargon, translated

The carrier paperwork uses a lot of terms that aren't obvious. Here's the cheat sheet: Premium, Liability, Coverage Limit, Claim, Exclusion, Additional Insured, and Certificate of Insurance, all in plain English. (Screenshot it for when your venue's vendor packet starts throwing terms at you.)

Infographic courtesy of Insurance Canopy.

Photographer vs Videographer, bundle or separate

Here's a thing most couples don't know and most photographers learn the hard way: an insurance carrier underwrites your policy based on what you tell them you do. If you applied as a "wedding photographer" only, your video work isn't covered. A claim from a videography incident, tripod cable that takes down a guest, audio recorder that damages a sound system, drone that hits a venue chandelier, gets denied because your policy didn't disclose the videography work.

Some carriers bundle photography and videography under one policy automatically. Most don't. The fix is straightforward: when you apply or renew, tell the underwriter explicitly that you do both photo AND video. Ask them to confirm in writing that the policy covers both. If they don't, ask for a rider or a separate videography line.

For couples shopping vendors: if the same person is shooting your photos and your wedding film, ask whether their insurance covers both services. The answer should be yes with no hesitation. If they have to think about it, that's a flag.

The two clauses your venue is probably asking for

Most venues want two specific things written into the COI. They'll spell it out in their vendor requirements packet. If your photographer doesn't already know what these mean, that's a flag.

Additional Insured

The venue is named on the photographer's policy as a covered party for your event. If something goes wrong during the wedding, photographer's flash unit overheats and starts a small fire, light stand falls and damages a table, gear bag trips a guest. The photographer's insurance protects the venue from being sued for it. Without this clause, the venue's own insurance would have to absorb it, which is why they require it.

Waiver of Subrogation

Some couples spell this "subjugation", same idea, different word. Subrogation is when an insurance company pays out a claim and then turns around and sues the third party they think actually caused the damage to recover the money.

A "waiver of subrogation" clause means the photographer's insurance company gives up its right to come after the venue later, even if the venue arguably contributed to the incident. Venues require this so they're not stuck in litigation six months after a wedding because somebody's policy decided to chase its own losses.

This isn't something you negotiate. It's a yes-or-no question on the COI. Your photographer's carrier either includes it or doesn't.

How to coordinate with your venue's event coordinator

The event coordinator at your venue handles the paperwork side. They'll have a vendor requirements document, sometimes called a vendor packet. That lists exactly what every outside vendor needs to provide. Photographer, DJ, florist, planner, caterer, baker, hair, makeup. Each one might have different insurance requirements.

Your job is small but matters: get that document from the coordinator early, then forward it to your photographer with the wedding date and venue name. The photographer takes it from there.

What to ask the coordinator:

- What's the minimum liability coverage required for the photographer?

- Does the venue need to be named as Additional Insured?

- Do you require a waiver of subrogation?

- How far in advance do you need the COI on file?

- Who's the certificate holder (the venue's exact legal name + address)?

Forward those answers to your photographer. They'll handle the rest with their insurance carrier.

A timeline that actually works

The earlier you get this on the calendar, the less stressful it is. Here's the version that doesn't blow up at week 13:

- At venue contract signing: Ask for the vendor requirements document. File it in the same folder as your contracts.

- 90 days out: Forward the COI requirements to your photographer. Confirm they've received it.

- 30 days out: Photographer requests the COI from their insurance carrier.

- 14 days out: Photographer delivers the COI to the venue's event coordinator. CC you on the email so you have the paper trail.

- 7 days out: Confirm with the coordinator that the COI is on file. Don't assume.

- Wedding day: Photographer brings a printed copy in their gear bag. Belt and suspenders.

Red flags when you're hiring

Insurance is one of the cleanest tells for whether a photographer is running a real business or a side hustle. Watch for these:

- "I'll get insurance if your venue requires it." Translation: they don't have a policy. Buying short-term event coverage 30 days out is possible, but the rates for one-off coverage are bad and the carrier may not include the clauses your venue needs.

- "My homeowner's policy covers it." No, it doesn't. Homeowner's covers your house. Commercial photography requires commercial general liability, different policy entirely.

- Pricing that doesn't support overhead. If a photographer is charging $500 for a full wedding, they aren't paying $400-800/year for liability coverage. Look at the price floor and reverse-engineer whether real business expenses fit.

- Vague answers. A working pro can tell you their carrier name, their coverage amount, and their typical turnaround for a COI without thinking. Vague is fail.

Why this protects you, not just the venue

Most couples assume insurance is the venue's problem. It's not. Without proper coverage, if something goes wrong, a guest trips on a light stand, a flash kit damages a wall, an extension cord starts a fire. The venue or its insurance company can come after the next person in the chain. That includes the couple who hired the uninsured vendor.

A properly insured photographer absorbs that risk. Without insurance, the risk sits on the couple who hired the uninsured vendor.

Where photographers and videographers actually buy insurance

Couples don't buy this, your vendors do. But it helps to know what a real working pro is shopping for, and what to ask if a photographer hesitates when you bring it up. Here are the carriers we've researched, used, or seen most often in this industry. Listed alphabetically; we're not affiliated with any of them.

- Full Frame Insurance, specialty liability and equipment coverage built for photographers and videographers. Annual policies, instant COIs, photo+video bundling available.

- Hill & Usher (PhotoCare), long-running specialty broker for photographers. Liability + equipment under one policy. Trusted name in event photography circles.

- PPA (Professional Photographers of America), member benefit insurance that covers $15K of equipment plus liability for active members. Worth it if the photographer is already a PPA member.

- R.V. Nuccio & Associates, specialty insurance for event photographers and videographers. Long history in the wedding industry; quick COI turnaround.

- Thimble, short-term, on-demand event coverage. Useful for one-off events, not a substitute for an annual policy. App-based and fast.

- The Hartford, general small business liability. Broader than photography-specific but solid coverage with strong COI fulfillment.

A few of these (Full Frame, Hill & Usher, R.V. Nuccio) are specifically built for photo/video pros and will know exactly what your venue is asking for. The general carriers (The Hartford) cover the same risks but may need more handholding when an event coordinator asks for unusual riders.

This is reference material. Treat it as a starting point, not a recommendation. Every photographer's situation is different: coverage limits, equipment value, whether they shoot internationally, whether they have a studio space. A working pro picks based on their specific needs, often after talking to multiple brokers.

What we do

We're Manuel & Alma, a husband-and-wife wedding photography and videography team based in Indio, California. We carry full commercial general liability that explicitly covers both photo AND video work, plus equipment coverage on our gear. COIs in 24–48 hours, with venue-specific Additional Insured and Waiver of Subrogation language built in by default.

If you're at the contract stage with us. Or just researching what's normal, send us your venue's vendor requirements packet and we'll tell you upfront whether our policy covers everything they ask for. We also offer wedding film coverage as an add-on (+$3,000); same insurance, same COI, no extra paperwork on your end. Reach out here and we'll write back the same day, usually within a few hours.

Manuel & Alma · Wedding photography for the Coachella Valley